Manufactured stone veneer siding, a deck addition, and window replacements are some of the stronger investments you can make in your home. Shutterstock images

In a tight housing market, homeowners looking for more space or finer features may not have the option of moving. Therefore, many are finding ways to upgrade by tapping into the equity they hold in their home.

A renovation can be a stressful project, so while you should always be person-ally invested and love any changes you make, remodeling with a return, but remodeling with a return on investment in mind can be a smart strategy. Whether one is thinking about moving in the next few months or further down the road. Though this approach is an inexact science, in many instances, it’s savvy for homeowners to consider what buyers may want when planning home improvements.

Evergreen Credit Union is a reliable, local lender, and we want to share information on how lenders like Evergreen can help you create your dream home.

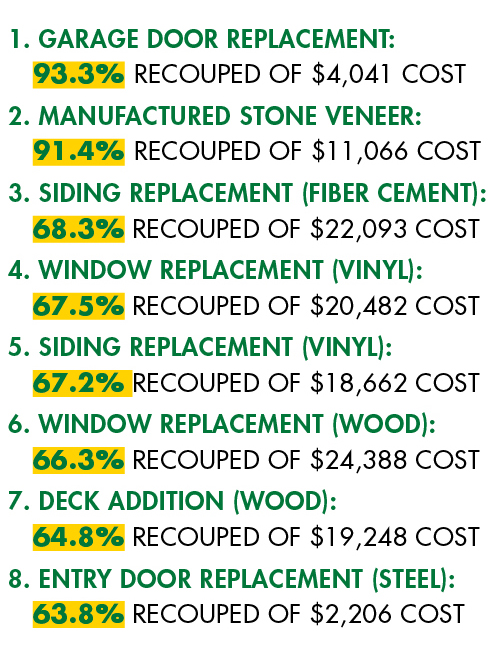

Homeowners may be surprised to learn which renovations garner the best ROI at resale. The home loan and refinancing company RenoFi indicates that overall, the average home improvement project provides 70 percent ROI. Many high-ROI projects add functional space and improvement. The following are some exterior renovations that help homeowners recoup the most money at resale, according to Remodeling magazine’s “2022 Cost vs. Value Report.”

Why are there no interior projects on this list? The only interior projects that cracked the Top 10 ROI for projects were a minor, midrange kitchen remodel or a midrange basement remodel, both of which have much higher investment costs than the projects here. (Remodeling magazine reports that a midrange basement remodel costing around $70,000 will provide a return of around $49,000—or 70 percent—at resale.) Though that’s not a poor return on investment, it required significant liquidity, plus interiors are often about personal preference and

FINANCING YOUR RENOVATIONS

Looking for liquidity to make home improvements? Homeowners generally have three choices when they borrow from a credit union or bank.

1. A traditional home equity loan gives a borrower a lump sum in return for fixed repayments over the life of the loan. This is also known as a second mortgage. Lenders will often let you borrow against a substantial percentage of your home when you use this product.

2. Instead of a lump sum, a home equity line of credit or HELOC approves the borrower for an overall credit limit that they can withdraw from as they need.

If you need liquidity to make home improvements, a HELOC can be more advantageous because in some cases, the interest paid on this loan could be tax-deductible. However, a HELOC typically carries a variable interest rate, so your monthly payments may fluctuate as time goes on.

Therefore, if you can come in under budget for your home renovations, that’s great. You may also be able to use excess funds in the credit line to consolidate other debts, but having equity in your home is a premium asset in a competitive real estate market.

3. If you have built significant equity in your home, you could consider a cash out refinance, which is an entirely new loan that gives you the cash differential based on the current value of your home.

Comments are not available on this story.

Send questions/comments to the editors.