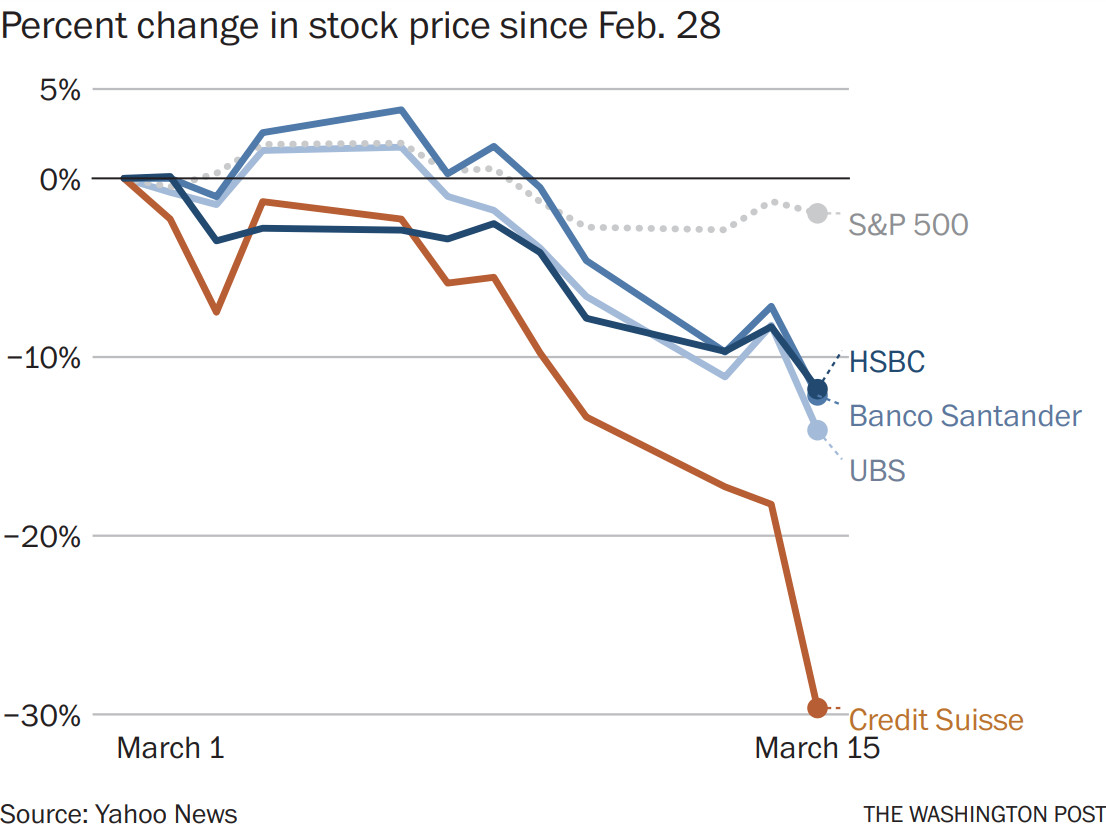

Fears for the stability of the global financial system rose Wednesday after Credit Suisse disclosed problems in its financial reporting and said it would tap more than $53 billion in aid from Switzerland’s central bank, raising turmoil in the markets in the wake of Silicon Valley Bank’s collapse.

The Swiss bank announced it would borrow from the Swiss National Bank late Wednesday, after its shares plunged on its disclosure that it had uncovered “material weaknesses” relating to its financial reporting. The Dow Jones industrial average fell by almost 1% Wednesday and European banking stocks tumbled, contributing to a 3% fall in the Pan-European Stoxx 600 index.

Compounding Credit Suisse’s problems, the bank’s largest investor, Saudi National Bank, signaled Wednesday that it would not be rushing in with more cash to help buttress the firm.

Credit Suisse has struggled with a host of problems for years, and its latest troubles differ from those that brought down SVB. But the Swiss bank is much larger and more integrated with the global financial system, and its problems come amid growing worries about bank stability globally.

“Credit Suisse is in principle a much bigger concern for the global economy than the regional U.S. banks which were in the firing line last week,” Andrew Kenningham, chief Europe economist with Capital Economics, said in a research note Wednesday. “Credit Suisse is not just a Swiss problem but a global one.”

The Swiss National Bank (SNB) and the country’s main financial regulator, known as FINMA, issued a joint statement late Wednesday saying that Credit Suisse “meets the capital and liquidity requirements imposed on systemically important banks.”

But “if necessary, the SNB will provide CS with liquidity,” the statement said.

Hours later, Credit Suisse said it would borrow from the Swiss central bank to “support Credit Suisse’s core businesses and clients.” It added that it would buy back up to $3 billion worth of debt.

Market jitters also continued to spark gyrations in bond trading Wednesday, causing an index measuring volatility in those markets to surge.

U.S. federal officials are trying to evaluate the extent to which U.S. banks may be vulnerable to a decline in Credit Suisse’s value, according to two people familiar with the matter, who spoke on the condition of anonymity to describe internal talks. That review was first reported by Bloomberg.

The Treasury Department declined to comment, although a spokeswoman confirmed in a statement that Treasury is monitoring the situation and is in touch with global counterparts. In addition to the risk posed by U.S. bank holdings of Credit Suisse’s stock, the Swiss bank has subsidiaries in the United States that fall under federal oversight and could pose financial risks.

The new questions around Credit Suisse’s financial stability could factor into the European Central Bank’s decision, scheduled for Thursday, about whether to raise interest rates.

In its annual report released Tuesday, the Swiss bank said it found “material weaknesses” relating to the bank’s “failure” to appropriately identify the risk of misstatements in its financial reporting. It added that it had failed to maintain effective monitoring over the bank’s “internal control objectives” and “risk assessment and monitoring objectives.”

The bank added that it did not “maintain effective controls over the classification and presentation of the consolidated statement of cash flows.”

Credit Suisse said it is working to address its problems, which could require it to “expend significant resources.” It cautioned that the troubles could ultimately impact the bank’s access to capital markets and subject it to regulatory investigations and sanctions.

The Swiss bank had delayed releasing its annual report after the U.S. Securities and Exchange Commission asked for more information last week about past cash flow statements.

The bank previously disclosed that it suffered significant customer withdrawals in October. It repeated that information in its annual report, saying “significant deposit and net asset outflows in the fourth quarter” undermined the bank’s full-year financial results. In December, bank Chairman Axel Lehmann told Bloomberg that the outflows “basically have stopped” and that some client money was returning, particularly in Switzerland.

If the Swiss bank were “to enter a really disorderly phase, that would be a big event,” said French economist Nicolas Véron, a senior fellow at the think tank Bruegel and at the Peterson Institute for International Economics. “Having said that, it was already perceived as troubled for some time. I expect that fact to have been factored into the strategies of market participants. So I imagine the risk won’t be borne by well-regulated institutions.”

The U.S. economy has appeared to be on strong footing in recent months, with the labor market remaining strong and inflation showing signs that it had begun to cool. But the outlook darkened Friday when Silicon Valley Bank suddenly failed, marking the second-biggest bank failure in U.S. history. The bank, which works with tech clients, got into trouble when its large holdings in U.S. government bonds fell in value as the Federal Reserve raised interest rates. Concerns about SVB’s health then sparked a run on deposits.

Financial stocks have been shaky ever since, and on Sunday regulators shuttered Signature Bank of New York. To stave off a broader panic, U.S. authorities stepped in to assure depositors at the failed banks they would not lose their money. Regional U.S. bank stocks fell sharply Monday and then rebounded Tuesday. But the Credit Suisse news Wednesday, a sign that banking-sector issues aren’t confined to U.S. banks, has rattled investors again.

Shares of First Republic Bank, another Bay Area bank catering to tech clients, dropped more than 16%, but rose again in after-hours market trading. Volatility spread across the market – the CBOE VIX index, known as Wall Street’s “fear gauge,” was up more than 10%.

The 167-year-old Credit Suisse was founded to finance the expansion of the Swiss railroads. Today it focuses on banking services for wealthy clients, as well as asset management and investment banking.

Unlike Lehman Brothers, which collapsed suddenly in 2008 as people recognized the size of its off-book liabilities and businesses, Credit Suisse’s troubles have built over time as the bank has struggled with financial losses, risk and compliance problems, as well as a high-profile data breach. In recent years it suffered big losses from its relationships with the collapsed hedge fund Archegos and a failed financial firm called Greensill Capital.

The Swiss bank has been attempting to restructure its business for months, aiming to scale back its investment-banking business and moving money toward global wealth management, according to Fitch Ratings.

Kenningham, the economist, said it was unclear how far the Swiss bank’s troubles could spread.

“The problems in Credit Suisse once more raise the question whether this is the beginning of a global crisis or just another ‘idiosyncratic’ case,” he wrote. “Credit Suisse was widely seen as the weakest link among Europe’s large banks, but it is not the only bank which has struggled with weak profitability in recent years. Moreover, this is the third ‘one-off’ problem in a few months . . . so it would be foolish to assume there will be no other problems coming down the road.”

Just two months ago, David Herro, chief investment officer of Harris Associates, said the Chicago-based investment firm planned to stick with its stake in Credit Suisse. The Swiss bank’s new chief executive, Ulrich Körner, was “very capable,” Herro said in a Bloomberg Television interview. “He’s the exact answer to their problems.”

But Herro added that he was losing patience. Ten days ago, Harris Associates sold its remaining shares.

The new market volatility could accelerate the U.S. recession that many analysts have predicted is looming, Deutsche Bank chief U.S. economist Matthew Luzzetti said Wednesday.

Previously, Luzzetti had forecast that the United States would enter a recession as soon as the end of this year. He now has a “higher conviction” in that forecast, he told The Washington Post.

“We’re a few days into seeing this volatility, and being able to see how this plays out is impossible at this point.”

The White House scrambled over the weekend to calm customers and the banking industry, moving swiftly in an effort to avert a sense of crisis. In Silicon Valley, start-up founders who kept their money at Silicon Valley Bank fretted over how they would pay their employees before breathing a sigh of relief when they learned they’d have access to their full accounts.

But SVB and Signature’s closures still sent a sense of precariousness through the banking sector. When Credit Suisse issued its annual report that found that its “disclosure controls and procedures were not effective” during a certain time period, it was into a market that was already on edge.

Credit Suisse’s largest investor, Saudi National Bank, which owns 9.88% of the Swiss institution, said it would not take a larger stake.

“The answer is absolutely not, for many reasons outside the simplest reason, which is regulatory and statutory,” Chairman Ammar Al Khudairy told Bloomberg TV.

Qatar’s sovereign wealth fund is another large investor in Credit Suisse, with a 6.8% stake.

The Washington Post’s Jeff Stein and David J. Lynch contributed to this report.

Send questions/comments to the editors.